California drivers can reduce SR-22 insurance costs through smart policy management and clean driving.

Introduction

If you’ve been told you need an SR-22 in California, you’re not alone.

Each year, thousands of drivers in California must file an SR-22 after:

- DUI convictions

- Driving without insurance

- License suspensions

- Multiple traffic violations

An SR-22 is not insurance itself.

It’s a certificate proving you carry the minimum required liability coverage.

But in California, the cost impact can be substantial.

This guide covers:

- 2026 SR-22 requirements

- Filing period rules

- Average costs

- Cheapest companies

- License reinstatement process

- How to lower rates faster

What Is an SR-22 in California?

An SR-22 is a financial responsibility filing submitted to the

California Department of Motor Vehicles.

Your insurance company files it electronically to prove you carry at least the state minimum liability limits.

It is required after high-risk driving violations.

California Minimum Liability Requirements (2026)

California requires:

- $15,000 bodily injury per person

- $30,000 bodily injury per accident

- $5,000 property damage

However — these minimums are extremely low.

Most insurers recommend increasing limits to:

- 50/100/50 or higher

Higher limits often only increase premiums modestly — and offer far better protection.

How Long Is SR-22 Required in California?

Typically:

- 3 years from reinstatement date

However:

- DUI-related cases may require longer monitoring

- Court-ordered filings can override standard timelines

Always confirm your exact requirement with the DMV.

Average SR-22 Insurance Cost in California (2026)

California is one of the more expensive states for high-risk insurance.

Estimated Annual Premiums

| Scenario | Avg. Annual Cost |

|---|---|

| Clean Driver | $1,900 |

| After DUI | $4,000 – $5,500 |

| After No Insurance | $2,800 – $3,800 |

| Multiple Violations | $5,500+ |

SR-22 filing fee: typically $15–$25.

But the surcharge from the violation is what drives cost.

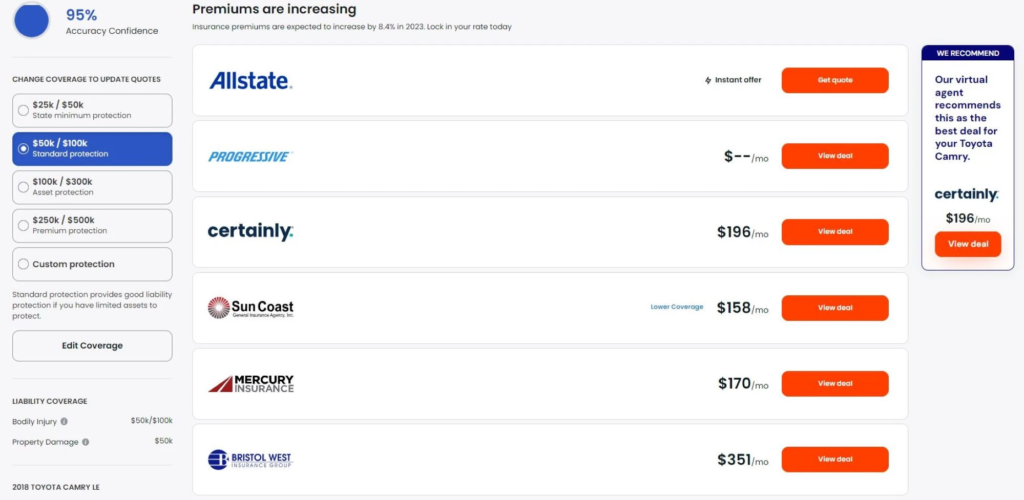

Cheapest SR-22 Insurance Companies in California

While rates vary by ZIP code, companies that often price competitively include:

- Progressive

- GEICO

- National General Insurance

- The General

Drivers in Los Angeles, San Diego, and Sacramento may see different pricing tiers.

Shopping is essential.

Steps to Reinstate Your License in California

- Complete court requirements

- Pay reinstatement fee

- Obtain insurance

- Have insurer file SR-22

- Confirm DMV compliance

Reinstatement fees vary based on violation type.

Never cancel coverage before the 3-year requirement ends.

A lapse can restart the clock.

Non-Owner SR-22 in California

If you don’t own a car but must file:

A non-owner SR-22 policy may be required.

It provides liability coverage when driving vehicles you do not own.

Average cost:

$500 – $1,200 per year depending on violation history.

How to Lower SR-22 Insurance in California

Re-Shop Annually

Risk tiers change yearly.

Improve Insurance Credit Score

California does NOT allow credit-based insurance scoring.

This is important.

Unlike many states, California uses:

- Driving record

- Years licensed

- Mileage

- Vehicle type

Credit improvement won’t reduce California auto rates directly.

That makes safe driving even more critical.

Raise Deductibles

May reduce comprehensive/collision costs.

Consider Usage-Based Programs

Telematics programs reward safe driving behavior.

Maintain Continuous Coverage

Gaps increase rates dramatically.

DUI in California: Additional Requirements

DUI cases may also require:

- DUI education programs

- Possible ignition interlock device

- Court fines exceeding $1,500+

Total financial impact often exceeds $15,000 over several years.

Insurance is only one part of the equation.

Cost Recovery Timeline in California

| Years Since Violation | Premium Outlook |

|---|---|

| Year 1 | Highest |

| Year 2 | Slight decrease |

| Year 3 | Moderate improvement |

| Year 4–5 | Noticeable recovery |

| Year 6+ | Near standard tier |

California insurers heavily weight violation recency.

Clean driving matters more than almost anything else.

What Happens If You Let SR-22 Lapse?

If your policy cancels:

- Insurer notifies DMV

- License may be suspended again

- Filing period may restart

- Reinstatement fees apply

Never let coverage lapse.

Is FR-44 Required in California?

No.

FR-44 filings apply in states like:

- Florida

- Virginia

California only uses SR-22.

Final Thoughts

SR-22 in California is manageable — but expensive if handled incorrectly.

Key takeaways:

- Filing typically lasts 3 years

- Costs vary widely by violation type

- Shopping is essential

- Continuous coverage is critical

- Clean driving accelerates recovery

The filing ends.

The financial recovery continues.

But with structure, costs decline steadily over time.