Understanding SR-22 insurance requirements and who must file them.

Introduction

SR-22 insurance requirements are a fundamental part of U.S. motor vehicle law and insurance regulation. Although the term “SR-22 insurance” is widely used, an SR-22 is not an insurance policy. Instead, it is a state-mandated legal filing that verifies a driver’s compliance with minimum auto liability insurance laws.

SR-22 requirements typically apply to drivers classified as high-risk due to serious traffic violations, court orders, or repeated insurance noncompliance. Because enforcement involves state Departments of Motor Vehicles (DMVs), insurance carriers, and courts, failure to comply can result in immediate and severe legal consequences.

This comprehensive guide explains SR-22 insurance requirements from a legal perspective, covering DMV regulations, court-ordered SR-22 obligations, state-by-state differences, compliance periods, and removal rules. It is designed to serve as an authoritative legal reference for drivers, attorneys, and insurance professionals in the United States.

What Is SR-22 Insurance?

SR-22 insurance is a state-required certificate of financial responsibility filed by an insurance company with the Department of Motor Vehicles (DMV). It confirms that a driver maintains the minimum auto liability insurance coverage required by state law and agrees to keep that coverage continuously for a specified period.

An SR-22 is not insurance coverage itself. Instead, it is a legal verification mechanism that allows the state to monitor a driver’s insurance status in real time.

Key characteristics of SR-22 include:

- Filed electronically by an authorized insurance company

- Required only for certain drivers, not the general public

- Tied to the driver, not necessarily to a specific vehicle

- Subject to strict continuous coverage rules

If the insurance policy associated with an SR-22 is canceled or lapses, the insurer must immediately notify the DMV, often triggering automatic license suspension.

Why Is SR-22 Insurance Required?

SR-22 insurance is required because the state has determined that a driver poses an increased financial risk on the road. The purpose of the SR-22 requirement is to ensure that drivers with a history of serious violations remain insured at all times.

Common legal reasons for SR-22 requirements include:

- DUI or DWI convictions

- Driving without auto insurance

- Involvement in an uninsured accident

- Reckless or negligent driving

- Accumulation of excessive violation points

- Repeated license suspensions or revocations

From a legal standpoint, SR-22 functions as a risk-control and enforcement tool. It does not punish past behavior directly but ensures future compliance with insurance laws.

DMV Authority and SR-22 Enforcement

DMV Legal Authority

State DMVs derive their authority to require SR-22 filings from state motor vehicle codes and insurance statutes. These laws authorize the DMV to condition driving privileges on proof of financial responsibility.

The DMV has the power to:

- Require SR-22 filings

- Monitor insurance status electronically

- Suspend or revoke driver’s licenses

- Impose reinstatement fees and penalties

How DMVs Enforce SR-22 Compliance

DMVs use electronic insurance monitoring systems that receive real-time updates from insurers. Once an SR-22 is filed, the driver is placed under continuous compliance monitoring.

DMV enforcement typically includes:

- Automatic suspension upon policy cancellation

- Mandatory reinstatement fees

- Extended SR-22 filing periods after violations

- Additional administrative penalties

Because enforcement is automated, even brief lapses in coverage can result in immediate consequences.

What Is a Court-Ordered SR-22?

A court-ordered SR-22 is an SR-22 requirement imposed directly by a judge, usually as part of a criminal or traffic-related case. Court-ordered SR-22 obligations often arise from DUI convictions or serious traffic offenses.

SR-22 as a Judicial Condition

Courts may require SR-22 as:

- A condition of probation

- A term of sentencing

- A prerequisite for license reinstatement

- A condition of plea agreements or diversion programs

When imposed by a court, SR-22 becomes a binding judicial order, not merely an administrative DMV requirement.

Consequences of Violating a Court-Ordered SR-22

Failure to comply with a court-ordered SR-22 may lead to:

- Contempt of court

- Extended probation periods

- Additional fines

- Incarceration

- Delayed license restoration

Court authority may override standard DMV timelines, meaning drivers must satisfy court requirements even if DMV obligations have technically ended.

SR-22 and Minimum Auto Insurance Laws

SR-22 filings enforce compliance with state minimum auto liability insurance laws. While coverage requirements vary by state, most mandate at least:

- Bodily Injury Liability per person

- Bodily Injury Liability per accident

- Property Damage Liability

SR-22 does not change the required coverage amounts unless the state mandates higher limits for specific violations. However, alternative filings such as FR-44 often require significantly higher coverage limits.

Insurance companies are legally obligated to notify the DMV immediately if coverage lapses, making uninterrupted coverage essential.

SR-22 Requirements by State

There is no federal SR-22 law. Each state independently defines its SR-22 requirements based on its insurance regulations and motor vehicle statutes.

Key Areas of State Variation

States differ in:

- When SR-22 is required

- How long SR-22 must be maintained

- Minimum liability limits

- Whether alternatives such as FR-44 apply

- Eligibility for non-owner SR-22

Examples of State-Specific Rules

| State | Typical Duration | Legal Notes |

| California | 3 years | Required after uninsured accidents and DUI |

| Texas | 2 years | Mandatory for license reinstatement |

| Florida | 3 years | FR-44 required for DUI convictions |

| Virginia | 3 years | FR-44 requires higher liability limits |

| Illinois | 3 years | SR-22 tied to Safety Responsibility Law |

Because SR-22 laws are state-specific, drivers moving between states must ensure interstate compliance.

What Is Non-Owner SR-22 Insurance?

Non-owner SR-22 insurance is designed for drivers who do not own a vehicle but are legally required to file an SR-22 to reinstate or maintain their driver’s license.

Legal Purpose of Non-Owner SR-22

Non-owner SR-22 policies:

- Provide liability coverage when driving borrowed or rented vehicles

- Satisfy state minimum insurance requirements

- Allow license reinstatement without vehicle ownership

Non-owner SR-22 does not cover vehicles owned by the driver or household members.

Most states recognize non-owner SR-22 filings as legally valid, making them a cost-effective option for eligible drivers.

How Long Is SR-22 Insurance Required?

SR-22 insurance is typically required for 2 to 5 years, depending on:

- State law

- Nature of the violation

- Court involvement

- Driving history

Common SR-22 durations include:

- 2 years for administrative violations

- 3 years for DUI or uninsured accidents

- 5 years for repeat or aggravated offenses

Any lapse in coverage may reset the entire SR-22 period, even if the lapse was unintentional.

What Happens If SR-22 Coverage Lapses?

A lapse in SR-22 coverage is treated as a serious legal violation. Once coverage is canceled, the insurance company files an SR-26 notice with the DMV, indicating noncompliance.

Consequences may include:

- Immediate license suspension

- Additional reinstatement fees

- Restarted SR-22 filing period

- Higher insurance premiums

- Court sanctions if court-ordered

Because enforcement is automated, lapses are rarely overlooked.

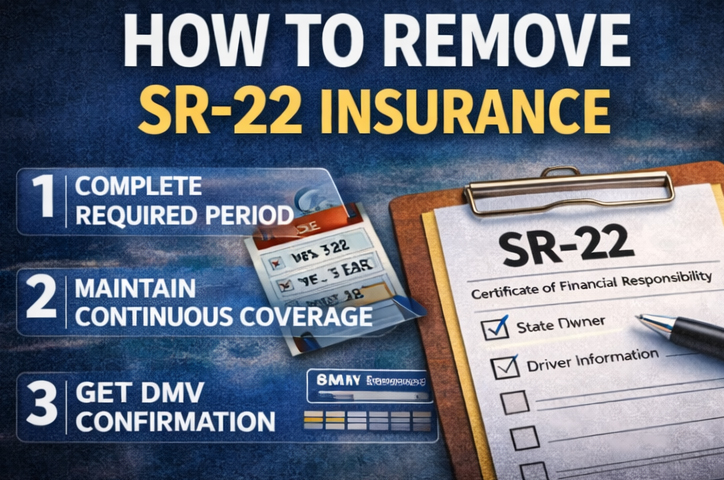

How to Remove SR-22 Insurance

SR-22 insurance can be removed only after all legal requirements are satisfied.

Legal Steps to Remove SR-22

To remove SR-22 insurance, a driver must:

- Complete the full state-required filing period

- Maintain continuous coverage without interruption

- Confirm eligibility with the DMV

- Instruct the insurer to remove the SR-22 filing

Drivers should never cancel SR-22 coverage without written DMV confirmation, as premature cancellation may reset the requirement.

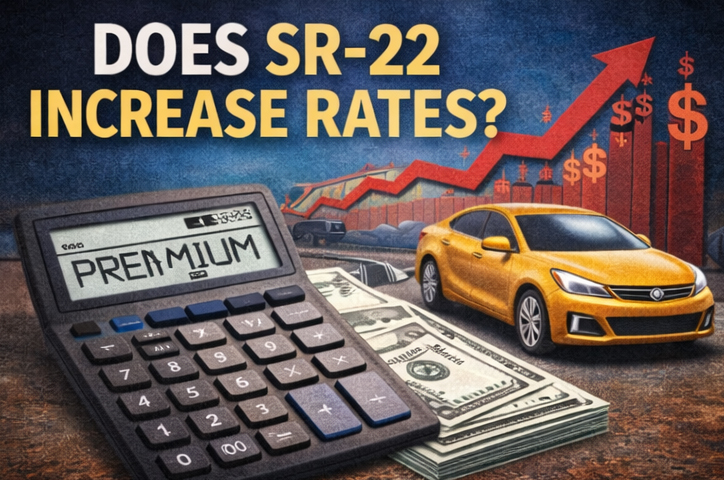

SR-22 and Insurance Rates

While the SR-22 filing fee itself is typically low, drivers required to file SR-22 often face higher insurance premiums. This increase is due to the underlying violation, not the SR-22 filing.

Factors affecting premiums include:

- DUI convictions

- Accident history

- Driving record severity

- State rating laws

Over time, maintaining a clean driving record can help reduce costs.

Frequently Asked Questions About SR-22 Insurance

Is SR-22 insurance required in every state?

No. Most states use SR-22, but some use alternative forms such as FR-44, and requirements vary by state law.

Can SR-22 be transferred between states?

Yes, but interstate compliance requires coordination between insurers and state DMVs.

Does SR-22 apply to the driver or the vehicle?

SR-22 applies to the driver, not the vehicle.

Is SR-22 permanent?

No. SR-22 is required only for a legally defined period.

Conclusion

SR-22 insurance requirements represent a complex intersection of insurance law, administrative enforcement, and judicial authority. Although commonly misunderstood, SR-22 is not insurance coverage but a legally enforceable mechanism that ensures financial responsibility among high-risk drivers.

Understanding how SR-22 works, how long it is required, and how to remain compliant is essential for maintaining lawful driving privileges in the United States. For drivers subject to SR-22 requirements, strict compliance is not optional—it is a legal obligation with significant consequences for failure.