SR-22 insurance is a certificate proving minimum auto liability coverage.

Introduction

The term **SR-22 insurance** is frequently encountered in discussions surrounding license suspensions, serious traffic violations, and high-risk drivers in the United States. Despite its widespread use, SR-22 insurance remains one of the most misunderstood concepts in the auto insurance and regulatory landscape. Many drivers incorrectly assume that SR-22 is a special or punitive type of insurance policy, while others believe it permanently classifies an individual as uninsurable. In reality, these assumptions reflect a fundamental misunderstanding of the legal and regulatory nature of SR-22.

This article provides a comprehensive, academically grounded, and search-engine-optimized explanation of **what SR-22 insurance is**, how it operates within state-level regulatory systems, and why it plays a critical role in enforcing financial responsibility laws. Rather than approaching the subject through fragmented questions or superficial summaries, this article presents SR-22 insurance as an integrated regulatory mechanism shaped by law, public policy, and insurance economics.By the end of this article, readers will have a clear, authoritative understanding of SR-22 insurance as a legal requirement, its implications for drivers, and its broader significance within the U.S. auto insurance framework.

Understanding the Meaning of SR-22 Insurance

At its most basic level, **SR-22 insurance** refers to a formal **certificate of financial responsibility** that is filed with a state motor vehicle authority by an auto insurance company. Importantly, SR-22 is **not an insurance policy**. Instead, it is a document that certifies that a driver maintains auto insurance coverage that meets or exceeds the minimum liability requirements mandated by state law.

The SR-22 filing establishes a legally binding assurance to the state that the driver is continuously insured. This assurance is not based on the driver’s personal promise or self-reporting, but rather on the insurer’s obligation to notify the state of any change in coverage status. As a result, SR-22 introduces an additional layer of regulatory oversight that does not exist in standard auto insurance arrangements.

From a definitional standpoint, SR-22 insurance is best understood as a **regulatory condition attached to an auto insurance policy**, rather than a separate product. The policy provides coverage; the SR-22 filing provides verification and enforcement.

The Legal Purpose of SR-22 Insurance in the United States

The legal foundation of SR-22 insurance lies in **state financial responsibility laws**. These laws require drivers to demonstrate the ability to pay for damages or injuries resulting from automobile accidents. While most drivers satisfy this requirement simply by purchasing standard liability insurance, certain drivers are subject to enhanced monitoring due to past violations.

SR-22 insurance exists to address situations in which a driver has demonstrated a pattern of non-compliance, unsafe behavior, or financial irresponsibility. From a regulatory perspective, SR-22 functions as a **risk control mechanism** that allows state authorities to ensure ongoing compliance without continuous manual enforcement.

The legal purpose of SR-22 insurance can be summarized in three core objectives:

1. **Ensuring continuous insurance coverage** among high-risk drivers

2. **Reducing the prevalence of uninsured driving**

3. **Protecting the public from uncompensated losses**

By shifting the responsibility for compliance monitoring to insurance providers, states are able to enforce insurance laws more efficiently and consistently.

How SR-22 Insurance Works Within State Regulatory Systems

When a driver is ordered to obtain SR-22 insurance, the requirement typically originates from a court ruling, a license suspension action, or an administrative determination by a state motor vehicle agency. Once imposed, the SR-22 requirement becomes a condition for maintaining or reinstating driving privileges.

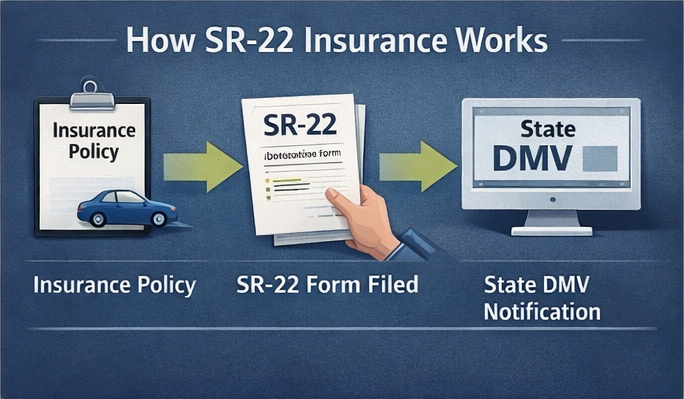

The operational process generally unfolds as follows. The driver purchases an auto insurance policy that satisfies the state’s minimum liability requirements. The insurer then files the SR-22 form electronically with the appropriate state authority. From that point forward, the insurer assumes a reporting obligation. If the policy remains active, the state considers the driver compliant. If the policy is canceled, lapses due to non-payment, or otherwise terminates, the insurer must immediately notify the state.This continuous reporting framework distinguishes SR-22 insurance from standard insurance arrangements. In effect, the insurer acts as a **regulatory intermediary**, ensuring that the state receives real-time information regarding the driver’s insurance status.

SR-22 Insurance Requirements and Minimum Coverage Standards

An SR-22 filing does not, by itself, dictate the structure of insurance coverage. Instead, it certifies that the driver carries at least the **minimum liability insurance required by state law**. These minimums are typically expressed as three numerical values representing bodily injury liability per person, bodily injury liability per accident, and property damage liability.

While SR-22 insurance does not automatically require higher coverage limits, some states impose enhanced minimums for drivers subject to SR-22 requirements. These higher thresholds reflect the state’s assessment of increased risk associated with prior violations.It is also important to note that SR-22 insurance generally applies only to **liability coverage**. Comprehensive and collision coverage remain optional unless required by a lender or leasing agreement. The regulatory focus of SR-22 is not on protecting the insured driver’s vehicle, but on ensuring that third parties are financially protected.

Circumstances That Lead to an SR-22 Insurance Requirement

SR-22 insurance is most commonly required following serious or repeated violations of traffic or insurance laws. These violations signal to regulators that standard compliance mechanisms may be insufficient.

Typical circumstances that lead to an SR-22 requirement include driving under the influence of alcohol or drugs, operating a vehicle without valid insurance, license suspension or revocation, reckless driving convictions, and multiple at-fault accidents within a defined period. While the specific criteria vary by state, the underlying rationale remains consistent: SR-22 is imposed when a driver’s behavior indicates a heightened probability of future risk.In this sense, SR-22 insurance is not arbitrary. It is the product of a regulatory assessment based on documented driving history and legal outcomes.

SR-22 Insurance and High-Risk Driver Classification

Drivers required to obtain SR-22 insurance are often categorized by insurers as **high-risk drivers**. This classification has significant implications for underwriting, pricing, and policy availability. High-risk designation is not based on the SR-22 filing itself, but on the violations that triggered the requirement.

From an actuarial perspective, insurers rely on historical data to assess the likelihood of future claims. DUI convictions, uninsured driving, and repeated violations are statistically correlated with higher loss frequencies. As a result, drivers subject to SR-22 requirements often face higher insurance premiums.However, it is essential to distinguish correlation from causation. SR-22 does not increase insurance rates; the underlying risk factors do. Over time, drivers who maintain compliance and demonstrate improved behavior may see their premiums decrease, even while the SR-22 requirement remains in effect.

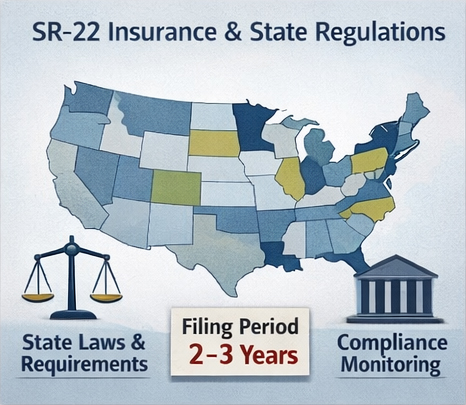

State-Level Differences in SR-22 Insurance Regulations

SR-22 insurance is governed entirely at the state level, resulting in significant variation across jurisdictions. Differences may arise in the duration of the SR-22 requirement, the types of violations that trigger it, and the administrative procedures for filing and termination.

Most states require SR-22 insurance for a period of approximately three years, though shorter or longer durations may apply depending on the severity of the offense. Some states allow alternative forms of financial responsibility, such as cash deposits or surety bonds, while others rely almost exclusively on insurance-based filings.These variations reflect broader differences in state regulatory philosophies and enforcement priorities. For drivers who relocate across state lines, understanding these distinctions is critical, as SR-22 obligations often remain tied to the original issuing state.

The Economic Impact of SR-22 Insurance

The financial implications of SR-22 insurance extend beyond the filing fee itself, which is typically modest. The more substantial economic impact arises from higher insurance premiums, license reinstatement fees, and potential indirect costs such as limited insurer choice.

From an economic perspective, SR-22 insurance operates as a **risk-based pricing mechanism**. By requiring high-risk drivers to maintain verifiable coverage, the system aligns insurance costs more closely with expected loss probabilities. This approach is consistent with broader principles of insurance economics and risk allocation.While the short-term costs may be significant, the long-term financial impact depends largely on driver behavior. Improved compliance and safer driving can mitigate premium increases over time, reducing the overall burden.

SR-22 Insurance for Drivers Without Vehicle Ownership

SR-22 insurance requirements apply to individuals, not vehicles. As a result, drivers who do not own a car may still be required to obtain SR-22 insurance. In such cases, a **non-owner SR-22 policy** is typically used.

Non-owner SR-22 insurance provides liability coverage when the insured driver operates a vehicle they do not own, such as a borrowed or rented car. While it does not cover physical damage to the vehicle, it satisfies the state’s financial responsibility requirements and fulfills the SR-22 filing obligation.These policies are often less expensive than standard owner policies, making them a practical solution for individuals who need to maintain compliance without regular vehicle use.

Compliance, Monitoring, and Policy Lapses

One of the defining features of SR-22 insurance is its strict compliance framework. Any lapse in coverage, regardless of duration or cause, triggers immediate notification to the state. This notification typically results in license suspension and may reset the SR-22 filing period.The compliance structure reflects the preventive intent of SR-22 regulation. By eliminating gaps in coverage, states reduce the risk of uninsured driving and reinforce accountability. For drivers, this means that maintaining uninterrupted coverage is not merely advisable, but legally essential.

Long-Term Effects of SR-22 Insurance on Drivers

Beyond its immediate legal and financial consequences, SR-22 insurance can have lasting effects on driver behavior and risk perception. The requirement to maintain continuous coverage under regulatory scrutiny often encourages greater adherence to traffic laws and insurance obligations.From a policy standpoint, SR-22 insurance represents a balance between deterrence and rehabilitation. It imposes consequences for past violations while providing a structured pathway back to full driving privileges. In this way, SR-22 contributes to broader road safety objectives without permanently excluding individuals from lawful driving.

The Role of SR-22 Insurance in Public Safety and Risk Management

Viewed within the broader context of public safety, SR-22 insurance serves as a targeted intervention aimed at reducing systemic risk. By focusing regulatory attention on drivers with elevated risk profiles, states allocate enforcement resources more efficiently.The SR-22 framework also reinforces the social contract underlying auto insurance systems. It emphasizes that the privilege of driving carries financial responsibilities, particularly when past behavior has demonstrated potential harm to others.

Conclusion

SR-22 insurance is best understood not as a specialized insurance product, but as a **state-mandated regulatory filing designed to enforce financial responsibility among high-risk drivers**. Rooted in financial responsibility laws and supported by insurer reporting obligations, SR-22 insurance plays a critical role in ensuring continuous coverage and protecting the public from uninsured losses.

While SR-22 requirements can be costly and administratively demanding, they serve a clear legal and policy purpose. By providing a structured mechanism for compliance monitoring, SR-22 insurance contributes to safer roads, more stable insurance markets, and greater accountability within the driving population.A clear and accurate understanding of what SR-22 insurance is—and how it functions—allows drivers, insurers, and regulators to navigate this requirement with clarity, professionalism, and confidence.