SR-22 After DUI: Filing requirements, insurance costs, and how to stay compliant after a DUI conviction

Driving under the influence (DUI) is one of the most serious traffic violations in the United States. Beyond fines, license suspension, and possible jail time, a DUI conviction often triggers an additional legal requirement: SR-22 insurance. For many drivers, the SR-22 requirement becomes one of the most confusing and financially stressful consequences of a DUI.

This guide explains what SR-22 after DUI means, why states require it, how to get SR-22 after a DUI, and how to find affordable coverage even with a high-risk driving record. Whether you own a vehicle or need a non-owner policy, this article is designed to help you meet legal requirements while minimizing long-term costs.

What Is SR-22 and Why Is It Required After a DUI?

An SR-22 is not an insurance policy itself. It is a state-mandated certificate of financial responsibility filed by an insurance company with the Department of Motor Vehicles (DMV) or equivalent agency. The SR-22 confirms that you carry at least the minimum auto liability insurance required by law.

After a DUI conviction, states consider the driver high risk due to impaired driving behavior. To reduce repeat offenses and protect the public, many states require SR-22 insurance after DUI conviction before reinstating or maintaining driving privileges.

Key points to understand:

- SR-22 proves continuous insurance coverage

- Your insurer must notify the DMV if coverage lapses

- Failure to maintain SR-22 results in license re-suspension

- The requirement typically lasts multiple years

Situations That Trigger SR-22 After a DUI

A DUI does not automatically require SR-22 in every case, but it commonly applies under the following circumstances:

- First-time DUI with license suspension

- Multiple DUI convictions

- DUI involving injury or property damage

- DUI combined with driving without insurance

- Refusal to submit to a breathalyzer or chemical test

In these scenarios, the DMV requires proof that you remain insured at all times, which is why SR-22 insurance after DUI conviction becomes mandatory.

DUI SR-22 Filing Requirements by State

SR-22 laws are governed at the state level, meaning requirements vary significantly across the U.S. Understanding DUI SR-22 filing requirements by state is critical to staying compliant.

Examples of State Differences

- California: SR-22 typically required for 3 years after DUI

- Florida & Virginia: Use FR-44 instead of SR-22 with higher limits

- Texas: SR-22 required after DUI-related license suspension

- Arizona: SR-22 required for 3 years; longer for repeat offenses

Some states do not require SR-22 at all, while others impose extended durations for repeat violations.

Important: You must file SR-22 in the state where your license is issued, even if you live or drive elsewhere.

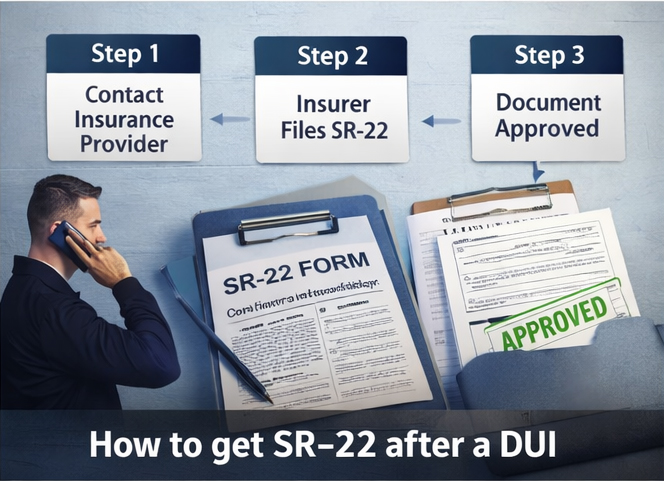

How to Get SR-22 After a DUI (Step-by-Step)

Many drivers mistakenly believe SR-22 is complex or handled by the DMV. In reality, the process is straightforward when you know what to do.

Step 1: Contact an Insurance Provider That Files SR-22

Not all insurers offer SR-22 filings, especially after DUI. Look for companies that specialize in high-risk drivers.

Step 2: Purchase or Modify a Policy

You can add SR-22 to:

- A standard auto policy (vehicle owners)

- A non-owner policy (drivers without a car)

Step 3: Insurer Files SR-22 With the State

Your insurance company electronically files the SR-22 with the DMV on your behalf.

Step 4: Pay Filing Fees

Most insurers charge a one-time filing fee, usually between $15 and $50.

Step 5: Maintain Continuous Coverage

Any lapse—even one day—can restart your SR-22 requirement period.

This process fully answers the question of how to get SR-22 after a DUI while avoiding common compliance mistakes.

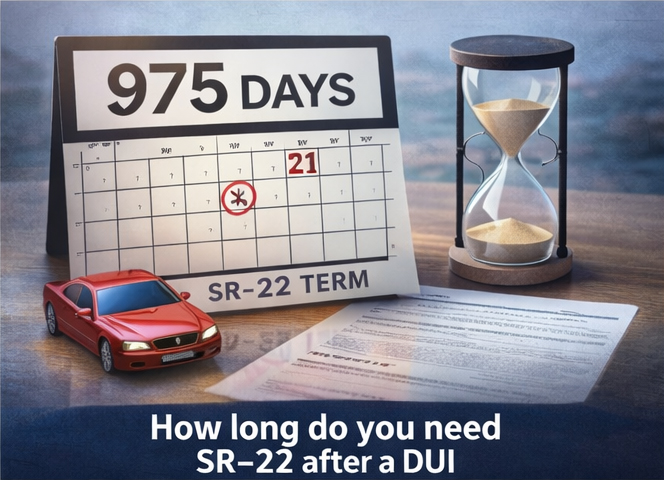

How Long Do You Need SR-22 After a DUI?

One of the most common concerns drivers have is duration. How long do you need SR-22 after a DUI depends on multiple factors:

- State law

- Severity of DUI

- Prior offenses

- Whether your license was revoked or suspended

Typical Timeframes

- First DUI: 2–3 years

- Repeat DUI: 3–5 years or longer

- Aggravated DUI: Up to 10 years in some states

The clock only runs while your SR-22 remains active. Any lapse restarts the requirement.

Cost of SR-22 Insurance After DUI

The cost of SR-22 insurance after DUI includes two components:

1. SR-22 Filing Fee

One-time fee: $15–$50

2. Increased Insurance Premium

A DUI dramatically increases your perceived risk, often leading to:

- 50%–200% higher premiums

- Policy reclassification as “high-risk”

Average Cost Impact

- Before DUI: $1,200/year (average)

- After DUI with SR-22: $2,500–$4,000/year

Costs vary by state, age, driving history, and insurer underwriting rules.

Cheapest SR-22 Insurance After DUI: How to Lower Costs

While SR-22 after DUI is expensive, there are proven strategies to find the cheapest SR-22 insurance after DUI.

Cost-Saving Tips

- Compare multiple insurers (not just major brands)

- Consider minimum liability coverage (if legally allowed)

- Choose a non-owner SR-22 policy if you don’t own a car

- Maintain a clean record during the SR-22 period

- Pay premiums in full to reduce installment fees

Shopping smart can reduce thousands of dollars over the SR-22 term.

Non-Owner SR-22 Insurance After DUI

If you don’t own a vehicle but still need to reinstate your license, non-owner SR-22 insurance after DUI is often the most affordable solution.

Who Should Consider Non-Owner SR-22?

- Drivers who sold their car after DUI

- Individuals who drive borrowed or rental vehicles

- Drivers seeking license reinstatement only

Benefits

- Lower premiums than owner policies

- Meets legal SR-22 requirements

- No coverage for vehicles you own

Important: Non-owner SR-22 does not cover vehicles you regularly use that belong to household members.

Best SR-22 Insurance Companies for DUI Drivers

Finding the best SR-22 insurance companies for DUI drivers requires focusing on insurers that actively underwrite high-risk policies.

Common Traits of Strong SR-22 Providers

- Willingness to insure DUI drivers

- Competitive high-risk pricing

- Fast electronic SR-22 filing

- Experience with multi-state requirements

Types of Companies to Consider

- Major national insurers (case-by-case acceptance)

- Regional insurers specializing in high-risk drivers

- Non-standard insurance carriers

Because underwriting rules change frequently, the “best” company varies by driver profile and state.

Common Mistakes to Avoid With SR-22 After DUI

Many drivers unintentionally extend their SR-22 requirement by making avoidable errors.

Frequent Errors

- Letting the policy lapse for non-payment

- Switching insurers without confirming SR-22 transfer

- Canceling SR-22 early without DMV confirmation

- Assuming SR-22 ends automatically

Always verify SR-22 removal eligibility with your DMV before making policy changes.

SR-22 After DUI vs Other Traffic Violations

Compared to speeding tickets or reckless driving, DUI-related SR-22 requirements are typically:

- Longer in duration

- More expensive

- More strictly monitored

This is why the “SR-22 After DUI” scenario is treated separately within the SR-22 by Situation category.

Frequently Asked Questions (FAQ)

Is SR-22 the same as full coverage?

No. SR-22 only proves minimum liability insurance, not comprehensive or collision coverage.

Can I get SR-22 without a car?

Yes. Non-owner SR-22 policies are designed specifically for this purpose.

Will SR-22 remove my DUI from my record?

No. SR-22 does not erase or reduce DUI penalties.

Final Thoughts: Navigating SR-22 After DUI Successfully

A DUI conviction significantly changes your insurance and legal obligations, but it does not permanently prevent you from driving. Understanding SR-22 insurance after DUI conviction, following state-specific filing rules, and choosing the right insurance strategy can help you regain compliance and control costs.By maintaining continuous coverage, avoiding lapses, and selecting the right policy type, most drivers successfully complete their SR-22 period and eventually return to standard insurance rates.